A Promising Budget With Missing Assurances

Zahid Hussain | 11 June 2022

In addition to the legacies, the FY23 budget faces several new challenges in the interplay between macroeconomic stress amidst post-pandemic recovery in a deeply uncertain global environment. The budget makers walked a tightrope with rising inflation and pressure on reserves.

They have come up with a few promising reforms incentivising export diversification and investments. The dazzling part is predominantly on the tax policy front. The budget makes a significant correction in the corporate tax regime overall, levelling the playing field within exports and denting the policy bias favouring inward orientation. It has the potential of triggering a new wave of green field investments in exports.

The missing promises are salient in budgetary allocation and in building resilience to the tail risks that have haunted countries and the world in recent years. The budget could be more measured on fiscal balances, better targeted on generosity, deeper in austerity, and more resolute on tax expenditures and evasions.

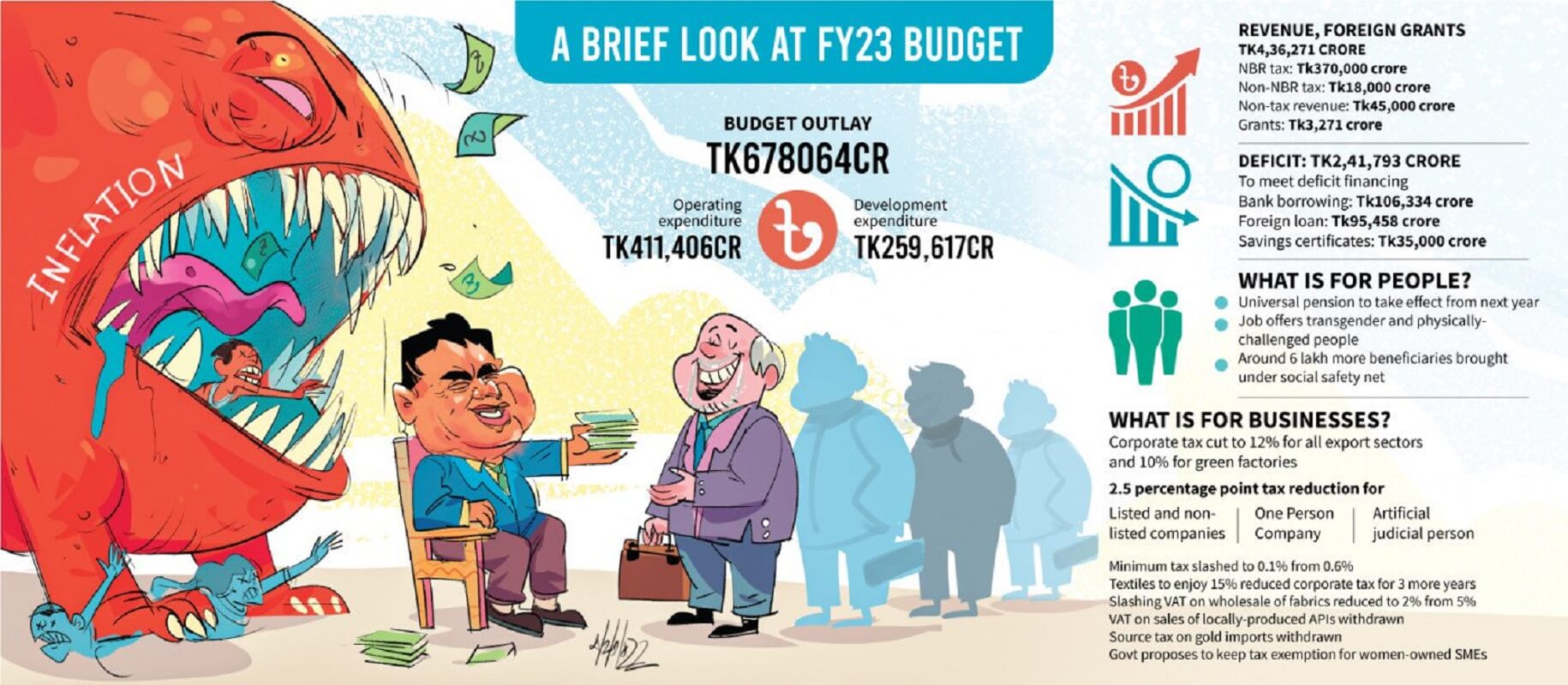

The budget has made a palpable shift in levelling the playing field between RMG and non-RMG exports. It proposes eliminating the Corporate Income Tax (CIT) differential between the two by reducing CIT on non-RMG exports from 30% to 12% for brown and 10% for green factories. Services export will be included in the definition of export in the tax statute. This should make non-RMG exports as attractive for investments as RMG from a CIT and incentive eligibility points of view, thus counterbalancing somewhat the incentive regime favouring import substitution. A level-playing field in customs-related services will further erase barriers to export diversification.

The above could be path changing in finally getting the "Made in Bangladesh" aspiration to mean what it really means – producing in Bangladesh for the domestic or international markets. The slogan is often used to justify inefficient import substitution. LDC graduation cannot be a ploy for enhanced protection in the run up to graduation which, if heeded, will waste the time available to local industries to prepare for competition without special and differential treatment.

The proposed 5% VAT on locally manufactured refrigerators, freezers and mobile handsets trading is another step correcting the inward orientation of the duty regime. Repealing tariffs on man-made fibre imports and a single rate of duty on the import of spare parts would have added to the competitiveness of Made in Bangladesh. Reduced VAT on yarn made from man-made fibre and other fibres are reduced from Tk6 per kg to Tk3 per kg.

The above steps forward come with a few backwards as well. The budget appears to have perpetuated a high degree of protection of domestic market-oriented industries through a plethora of increases in para tariffs on imports. The high level of protection provided through non-transparent para-tariffs has already created an enclave for industries catering to the domestic market due to relatively higher profitability. VAT and SD exemptions to Made for Bangladesh result in additional protection.

Cases in point in this budget are increases in VAT/SD exemptions to car manufacturing, production of compressors for refrigerators, API, battery, polythene bags, plastic bags, towels, bedsheets, textile grade pet chips, mobile phone batteries, power tiller and so on. The continuation of the existing six slabs of customs duty rates, 3% Regulatory duty on the products that have the highest import duty, and twelve slabs of supplementary duty rates, and increased import duties on a whole range of manufactured products misses another opportunity for reform to face post LDC challenges.

Walking the talk on incentivising investments

A few measures to ease the cash flow constraints on investments are noteworthy. Right or wrong, a consensus prevails that the CIT rate level is high and the structure complex. The "high" part of the consensus is music to the corporates while the complex part is partly their own making, intended or otherwise. Policy makers have responded to where the consensus is the strongest by slashing 500 basis points from the rates encompassing most of the large and medium corporate sector for three years in a row.

Corporate income tax rates are reduced by 250 basis points except for commercial banks, merchant banks, tobacco, and telecom companies. Listed, non-listed and one-person companies will come under the purview of the new tax cut subject to maintaining cashless transactions and publicly offloading at least 10% of shares in case of listed companies. The existing 15% corporate tax for the textile sector is extended for three more years. This is complemented with cutting tax at source on supplies of raw materials to manufacturers from 7% to 4% and trading goods from 7% to 5%, which reduces the effective tax rate. Minimum tax on startups is reduced from 0.6% to 0.1%. They are also exempt from the bindings of all other types of reporting except submitting income tax returns. Measures like this stimulate investment when investors are convinced that the changes will stick.

Some of the following might. These include amendments in the tax ordinance to reduce the required shareholdings in amalgamated companies from 90% to 75%; exemption of mergers from capital gains tax; carrying forward losses and depreciation of merged entities; and de jure legitimacy in tax returns for tax deductibility of expenditures on R&D. Foreign currency income by Bangladeshi flagged oceangoing ships is exempted from the current 10% CIT. Hikes in freight rates have renewed incentives for investments in ocean going vessels.

Deduction at source from interests on bank deposits of companies takes away some flavour from the effective rate cuts. The budget proposes raising the source tax to 20% from the existing 10% on interests on savings deposits, fixed deposits or any term deposits maintained by companies with banks or non-bank financial institutions.

A stronger motivation for investment induced by lower tax rates does not translate into action when inflation is rising, and reserves are stressed. Inflation and all the volatilities that come with it stretches the wait and see mood of the investors. Deeper investment climate reforms got the usual speech service. The budget overlooks a key driver of inflation and the dollar problem, thus falling short in prioritising macroeconomic stability.

Reticence to macroeconomic imbalances

Reducing inflation is listed as priority number one. It is largely assumed to be imported which blind sighted the budget somewhat to the role of domestic demand growth in the propagation of inflation. BBS data on growth of private consumption and imports provide convincing evidence on the rise in domestic demand. Only demand growth can explain simultaneous increases in GDP growth and inflation as projected for FY22 in the budget documents.

The assumption matters in shaping the policy response. Attributing the increase in inflation entirely to import cost push leans policy towards adaptation rather than mitigation because the cause is all external. Fiscal expansion as a risk to inflation takes a back seat since there is no domestic heat to extinguish. The budget has made a risky choice to err on the side of adding fuel to overheated domestic demand.

The primary budget deficit is projected to increase 23.6% relative to FY22 revised budget, miles ahead of the projected 5.6% inflation and rising from the revised 3.4% of GDP in FY22 to 3.7% in FY23 after ebbing at 1.7% in FY21. Fiscal policy remains on an expansionary course, instead of consolidation. If the consumption and import boom taper off naturally, the effect of deficit expansion may be muted. Yet by fuelling demand growth, the budget may delay disinflation if not exacerbate the momentum.

This is probably motivated by investment. But some things are a little amiss here. The total investment rate is projected to slip from 31.7% of GDP in FY22 to 31.5% and export growth to slow to 20% in FY23. Yet GDP growth rises from 7.3% in FY22 to 7.5% in FY23 while inflation decelerates to 5.5%. All these in a stagflationary world with slowing global trade and heightened levels of commodity prices. The likely acceleration in remittance inflows is the only significant tailwind in the horizon.

Higher growth with slower investment, exports and disinflation is possible with a shift in productivity growth. Indeed, the central justification for projecting higher growth in the Macroeconomic Statement is the opening of Padma Bridge (PB), Dhaka Metro Line-6 and the Karnaphuli Tunnel for public use. This is a little too much to hope from a single mega project like PB to deliver growth immediately. The opening of the other two in FY23 is still not known. The assumed sources of productivity growth are distant. The likelihood of a scenario in which growth is rising with falling inflation is hard to distinguish from wishful thinking under the likely global and domestic conditions in the near-term.

External stabilisation is not in the priority list. What matters for external balance is public expenditure on imports not financed externally. There is no obvious attempt to reduce allocations to import intensive domestically financed projects. Assuming the historic trend in shortfall in external financing targets, the budget is likely to add to demand for foreign exchange rather than syphoning it. Domestic financing of ADP is projected to grow 11.5% compared with 5.7% growth in project aid.

The question this year is not whether the projected expansion in deficit is achievable, the question is, should the government even strive to achieve them? We typically undershoot the deficit target. The extent of the undershooting is likely to matter more this time because of the pre-existing heat in domestic demand. Undershooting around historic trends means the deficit will expand at a time when demand deficiency is not the problem, unlike a year and a half ago. Domestic bank borrowing is projected to grow 21.8% relative to the upwardly revised FY22 budget target. These do not pose sustainability risk because of favourable debt dynamics with GDP growth exceeding the effective interest rate on debt. The issue is aggravation of pressure on inflation, exchange rate, and interest rates.

The elephant in the room

The elephant in the room on reforming the deployment of public resources this year is the subsidy regime broadly defined to include incentives and loans. Decision on the size of the subsidy is inextricably linked to decisions on administered prices of oil, gas, electricity, and fertiliser.

Passing on the cost increase fully in FY23, no matter how it is timed, will inevitably push inflation. Prices of these items are contagious, unlike say the price of meat or vegetables. Not passing on adds a significant burden on the budget. International commodity prices are not projected to decline anytime soon from their current elevated levels, posing a difficult balancing challenge to the budget makers.

They decided to do more of the same. Total subsidy in FY23 will rise 24% to Tk82,745 crore, constituting nearly one out of every 8 takas of total public expenditures, notwithstanding the recent 22.8% increase in the wholesale price of natural gas. The expansion in provision for subsidies to food, agriculture, and electricity are appropriate for mitigating the inflation risk. There is no reshuffling of subsidies.

The government could be more accommodative on subsidies if it were less accommodative on policy support. The size of allocation to "incentives" do not reflect any attempt at creative destruction. Incentives that were there (exports, remittance, cash loans) were expanded to Tk41,800 crore. There is no compelling reason for their continuity given the large recent depreciation of the taka and robust recovery in manufacturing.

Need to do better on targeting generosity

Inflation has damaged the real income, food security, and essential household expenditures of the low-income households in Bangladesh, mirroring a globally observed pattern. PPRC-BIGD surveyed almost 4,000 households in May this year. They find per capita daily incomes increased 27% from August 2021 to January 2022, reverting 6% between January and May 2022 due to inflation. Compared to last year, the purchase of "fair price rice" increased in May 2022, among both people below and above the poverty line.

Real incomes of poorer households were still 15% below pre-pandemic levels.

Income erosion in urban slums was over twice the erosion in rural areas. Households have drastically reduced consumption of fish, meat, milk, and fruit. Since February 2022, two-thirds of the households have reduced medical and children's education expenses. The households are adjusting quality to balance their budgets. A recent CPD calculation showed it costs a four-member household around Tk21,000 a month to provide for essential food items.

The additionally distressed livelihood of the low-income households warranted deeper attention beyond what exists in the Tk6,78,000 crore total expenditure budget for FY23. The Tk84,564 crore (14.2%) rise in expenditure relative to the FY22 revised budget needed to have a distribution tilted towards public expenditure in education, health, and social protection than the structure inherited from FY22.

The budget does not live up to this expectation. Growth in allocation to agriculture (38%), primary education (20.7%) and health (13%) are impressive. However, the government does not apparently feel the need for reprioritising the mega projects in the transport sector. The expenditure shares of the top ten economic sectors are difficult to square with the stated top seven "to do" budget priorities where agriculture and social protection get prominence—a case of not running the talk.

Allocation to health is 5.4% of total expenditures, same as in the FY22 budget. Bangladesh has managed to flatten the curve on Covid cases. As of June 2, 69.03% of the population received double vaccine doses, of whom 12.8% are boosted. Bangladesh has targeted to inoculate 70% of the population with two vaccine doses in line with the World Health Organization's target. There are reportedly enough doses in stock to get through the booster dose campaign. In the last two fiscal years, Tk10,000 crore was earmarked in the budget for vaccine procurement, of which Tk6,500 crore was spent. There is a block allocation of Tk5,000 crore in the FY23 budget to meet Covid related exigencies.

Stronger attention is needed to manage health expenditures better. The sector is notorious for failing to utilise the budgetary allocations. Delays in fund availability, recruitment and retention of human resources, procurement of drugs and medical supplies, and adequate provisioning for allocating operational funds at the facility level have remained the Achilles' heel in the Health Services Division. A major puzzle is why the problem is so acute in health, unlike the rest with the same administrative systems and culture.

Education's share is 14.7%, one percentage point lower relative to FY22 budget. Making up lost learning (1.5 years of schooling due to Covid) and reducing disparities are the biggest challenges. Inflation has added new significance to education because of its ability to reach the poor. The budget utilisation rate in the education sector is typically over 90%. The World Bank's benefit incidence analysis shows spending on education at the primary level reduces two times the gap in per student spending on primary education between the rich and poor households. The FY23 budget missed an opportunity to use the education budget for fighting inflation as well as making up lost learnings.

The Primary Education Stipend Program is a key contributor to progressivity at the primary level. Although PESP is now supposed to cover all children, about 2 in 5 children not receiving stipends are in the poorest quintile. A new school meal program, kit allowances, ICT teachers' training, adequate laboratory set-ups, and an internship program for graduates were some of the big announcements the government made in the FY22 budget. Sadly, we never get any explanation on the status of delivery in measures promised for the outgoing year in any developmental sector, not just education.

The budget envisages increasing coverage in social protection. The benefits provided by many programs represent 1 to 3% of total household income for the poor or extreme poor, except for few. The beneficiaries overwhelmingly prefer to receive their benefits in cash rather than food. Administrative costs of food transfer programs typically are almost 2.5 times higher than those of cash transfer programs.

Budget implementation in social assistance must draw lessons from the comparative experience in the recently introduced TCB Family Card system for 10 million urban low-income families and the Prime Minister's Tk2,500 cash assistance to the urban poor last year. Apparently, the overall satisfaction of those who purchased from TCB and received cash from the PM was high. However, two-thirds of the Family Card holders mentioned long queues as a big challenge in purchasing in the PPRC-BIGD survey. There is a block allocation of Tk5,000 crore to help the poor cope with natural shocks and a Tk20 crore grant for poor students.

Enhancing support to existing programs such as stipends, old age pensions, and cash transfers, where implementation capacity can be presumed to have improved, would have directed generosity to where it is needed the most.

Austere in austerity

The conflicts with austerity created by expanding expenditures could have been softened with cuts in allowances, travel, vehicles, training and so on. The government reportedly saved Tk9,000 crore in FY22. Expenditure on travel declined Tk1,066 crore, vehicle purchase Tk4,704 crore and supplies and services Tk1,200 crore. The pre-budget discourse exhorted doing better. The allocations paint a different picture.

Allocations for public pay and allowances have increased 9.6% relative to the revised budget, already well ahead of inflation after increasing 29% in the last three years when the cumulative inflation was about 20%. This looks blatantly inequitable when juxtaposed against a constant personal income tax exemption limit during the same period. Expenditures on travel and transfers, which increased 40% in the last three years, have increased 51.8%. Expenditure on training increased 45% in the last three years. In the budget, it has increased further by 22.1%. The best effort does not appear to have been made.

Development expenditures do not show any obvious signs of austerity. Allocation for projects outside the ADP has increased. The size of the Annual Development Program continues nearly the same as the budget deficit. There are no course corrections to respond to the stabilisation challenges through reprioritisation of several questionable, including some mega, projects. The planning minister had assured of revisiting all the 1800 or so ADP projects not just to save foreign currency expenditures or deflate domestic demand growth but also to shed obesity.

Revenues may continue to elude

The revenue growth target is a deceptively modest 11.3% relative to the FY22 revised budget target of Tk3,89,000 crore, the same as in the original budget. A shortfall in the latter is fait accompli, may be around Tk25,000 to 30,000 crore. The higher the shortfall, higher will the growth target for FY23 look. There are some measures providing hope and some that clip the wings of hope.

Increased source tax on export earnings from 0.5% to 1% will yield Tk5,500 crore out of the Tk44,000 crore projected increase in revenues if exports reach $60 billion. Over the past decade or so, almost every time the source tax was hiked, exporters were able to reverse it. The Bangladesh Garment Manufacturers and Exporters Association had recommended keeping the 0.5% rate unchanged for next five years. The source tax net is expanded while some rates have been reduced apart from the reduction on raw materials to manufactures and trading goods.

The increases and decreases in source taxes are likely to neutralise each other. The government appears to be betting on better tax compliance as the driver of revenue growth. A significant legal measure encouraging compliance is the rolling out of the special privileges in the onshore black money whitening facility. This rarely yielded the expected revenues and investments. The positive signal from this measure is negated by opening a new window for legalising unreported assets offshore without any question and prosecution next fiscal year subject to paying taxes.

There are a few administrative measures to improve compliance. TIN holders, yet to file their tax returns, will be exempted from paying fines for previous years if they file returns in FY23. There is a stiff fine under the income tax law on any person who fails to file a return without reasonable cause. The number of TIN holders is over 7.5 million, of which two-thirds do not file income tax returns.

There is an increased penalty for businesses not filing tax returns. Currently business entities are not required to file tax returns even if they have a TIN. Filing return will be mandatory in FY23 onwards failing which risks penalties ranging between Tk5,000 to Tk20,000. The Registrar of Joint Stock Companies and Firms has about 1.75 lakh registered companies, of which less than 30,000 submit returns.

The submission of audited financial reports by all business entities, defined as companies under the Income Tax Act, will be mandatory. Currently, only the businesses registered with the RJSCF are required to file audited financial statements. This may be problematic for small business entities.

Many TIN holders are reluctant to file returns fearing fines and harassment. The FY23 budget is experimenting with a mixture of decrease in fines for individuals and increase in fines for businesses. On the harassment part, the strategy appears to be to threaten more harassment as an alternative to less. NBR officials are empowered to snap utilities of tax defaulting businesses. The Deputy Commissioners of Taxes can take such actions to collect undisputed taxes. Current undisputed taxes amount to about Tk2,000 crore, compared with Tk34,000 crore clogged in legal battles.

Taxation of fish and poultry farming is harmonised with fish and poultry hatcheries under a single tax slab to plug tax evasion. This means tighter tax slabs for poultry and fish farming in FY23. Their tax exemption limit will be reduced from Tk20 lakh to Tk10 lakh followed by progressive rates similar to the tax in force for fish and poultry hatcheries.

Whether and to what extent the legal and administrative measures will expand the tax base and revenues are anyone's guess. The revenue gains from base expansion and several indirect tax rate increases need to outweigh the revenue losses from the direct and indirect tax decreases. At the end of the day, the revenue growth target will be at the mercy of growth in the nominal value of international trade, domestic manufacturing, and formal sector services. Enhanced revenues from imports due to exchange rate depreciation and international price increases, while sizable by themselves, are unlikely to provide significant additional mileage in achieving the revenue target.

The writer is an economist.

This article was originally published on The Business Standard.

Views in this article are author’s own and do not necessarily reflect CGS policy.